BiQ: Update For the Week Ending 10/17/25 (STXS, ABEO, TLX, KURA, DCTH, LXEO, RCEL)

Last week was very eventful, and there was a lot of discussion in BiQ Chat, so I wanted to share a few highlights to bring everyone up to speed.

Stereotaxis (STXS) issued a press release announcing a collaboration agreement with CardioFocus, Inc. to develop a PFA (Pulsed Field Ablation) catheter for use with the company's Genesis and GenesisX platforms. While the news seems to have gone mostly unnoticed, which isn't surprising as STXS continues to run mostly under the radar, I consider this a pretty big deal. PFA is rapidly gaining steam in the cardiac ablation market, and having a PFA catheter will provide support for Genesis and GenesisX.

Abeona Therapeutics (ABEO) issued a press release announcing that their ABO-503 GTx for X-linked Retinoschisis (XLRS) was selected by the FDA for its Rare Disease Endpoint Advancement Program. While any commercial launch of a GTx under this program is still at least two years away, inclusion in the highly competitive RDEAP will significantly accelerate clinical development. For context, the estimated prevalence of XLRS is around 35,000 patients across the US and EU, and there are currently no approved therapies.

Telix Pharmaceuticals (TLX) issued a press release pre-announcing Q3 revenue. the company also increased FY 2025 guidance, despite setbacks with the approvals of Pixclara and Zircaix. Although recent setbacks have been frustrating, my view is that Telix remains a high-quality company with top-notch management.

Kura Oncology (KURA) announced preliminary data from its ongoing P1 studies for its FTI (Farnesyl Transferase Inhibitor) programs. While the data is still very early and far from conclusive, my take is that the early data shows encouraging activity with manageable toxicity. The FTI programs remain a "call option" for now as the data is too early-stage to assign value to, but I am looking forward to future data updates.

It was a mixed bag for Delcath Systems (DCTH). On October 18th, the company announced positive results from its investigator-led CHOPIN clinical trial. While results are very encouraging, and shares reacted positively to the news, I don't expect these results to drive any significant near-term revenue; however, I do see them as a very positive proof-of-concept for future development.

Later the same day, DCTH pre-announced Q3 revenue, which came in well-below analyst estimates. Management attributed the revenue decline to NDRA discounts and summer seasonality. There's no denying that the revenue shortfall was disappointing, and I expect the market will react accordingly on Monday. However, I don't think one bad quarter changes the long-term picture in any meaningful way.

Lexeo Therapeutics (LXEO) announced a surprise public offering and concurrent private placement for an aggregate of approximately $145M. I commented in chat that I didn't see the capital raise as a negative given the strong pricing, and indeed, the market seems to have reacted favorably to the news as well (at least so far.)

Avita Medical (RCEL) has been a challenging stock for investors for quite some time. While I believe RECELL GO has tremendous potential, the company has, so far, failed to capitalize on it and has made several missteps along the way. Earlier in October, the company announced NTAP reimbursement for the use of RECELL with non-burn acute wounds, which I consider to be a positive development.

Last week, however, the company pre-announced approximately $17M in Q3 revenue. This was a very disappointing number, and a big miss versus both my and analyst's estimates. Needless to say, this is just another in a series of commercial missteps by the company. The only silver lining is that concurrently with the revenue announcement, the company also announced the departure of CEO Jim Corbett. I consider this to be a positive for the company, as there has obviously been a severe failure of leadership. I hope that Q3 represents a trough quarter for them, but only time will tell. In the meantime, RCEL remains on the BiQ Probation List.

Markets have been choppy lately, so stay safe, remember to keep the FOMO in check, and remain focused on only high-quality names at attractive valuations. Biotech investing is a marathon, not a sprint.

Here is a quick snapshot of the BiQ Active Portfolio. Note that there are currently 5 BiQAP names in the red; however, the thesis for each continues to progress, and I remain confident over the long term. BiQ Comprehensive Gain/Loss (inclusive of trading and option profits/losses over the investment period) is highlighted in green.

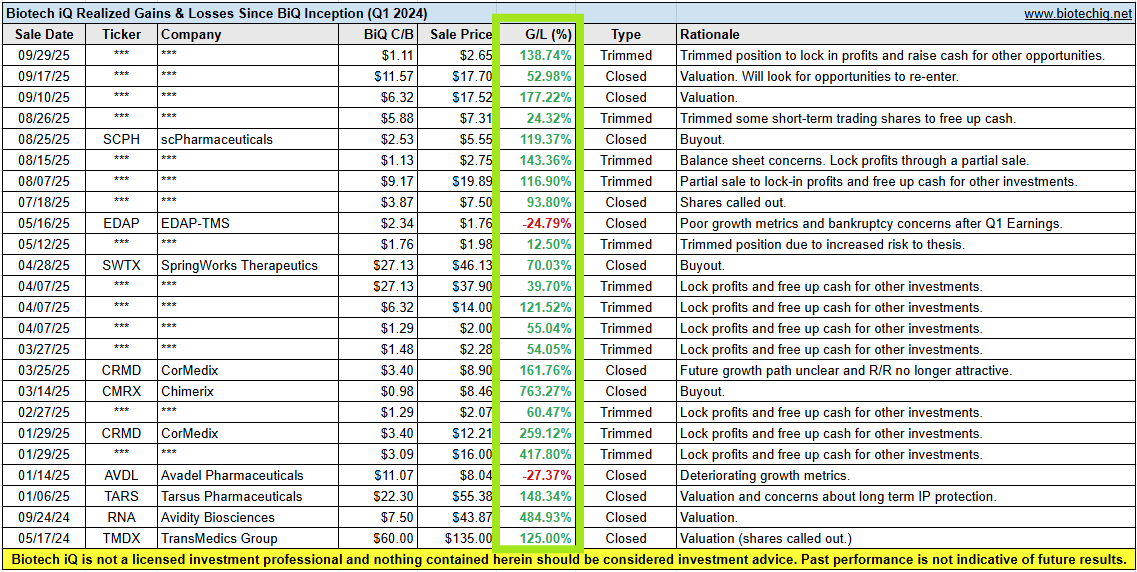

Below is a snapshot of the BiQ Past Performance spreadsheet, including some recently trimmed positions.

Please refer to the BiQAP Live spreadsheet on the Active Portfolio page for more information on any actively covered companies.

Not a BiQ Premium member, or have a friend who may be interested? Try BiQ Premium for $50 per month, or $250 (50% off) for the first year.

Biotech iQ is 100% subscriber supported. If you find this information helpful, please spread the word. You can also follow me on X @ Biotech iQ (_Biotech_iQ).

Biotech iQ is not an investment professional, and nothing on this page or this website should be considered investment advice. Please consult with a licensed investment professional as necessary. Past performance is not indicative of future results.

Member discussion