BiQ: Some Additional Thoughts on Iovance and Q1 Earnings (IOVA)

I spent some more time yesterday thinking about Iovance Biotherapeutics (IOVA) and its recent Q1 earnings release. Sometimes, or perhaps most of the time, it can be very difficult to tune out the noise and isolate the information that truly matters. After that, it can be even harder to interpret that information. This is one of the many factors that make biotech investing so challenging—but also rewarding if you get it right, and equally painful if you get it wrong.

In the case of IOVA, after considering Q1 earnings more closely, I believe I may have underestimated the risks associated with the investment. I still believe Amtagvi is a great product and can be successful in the long term, but the company faces significant challenges. Launching a new therapy or drug is always challenging, which is par for the course in biotech. A lot can go wrong with any launch. However, IOVA faces some unique challenges to adoption that are important to consider.

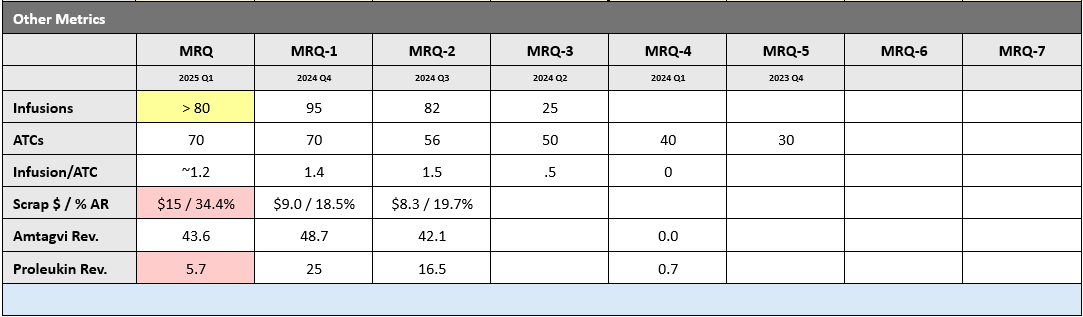

First, let's examine what went wrong in Q1. A good place to start is the Other Metrics section from the iQ Cheat Sheet.

As we can see, things seemed to be trending reasonably well up to Q4, with infusion volumes and Proleukin sales hitting all-time highs. However, the company hit a major speed bump (or perhaps pothole is a better description) in Q1, with both infusion volumes and Proleukin sales dropping from Q4 levels. There are three key insights to be learned from this analysis:

- IOVA's gross margins are currently almost completely dependent on Proleukin sales, which can be highly variable due to customer stocking.

- IOVA continues to face significant hurdles to adoption.

- Manufacturing and patient drop-out challenges continue to plague the company.

In the paragraphs below, let's examine each of these more carefully and explore what they could mean for IOVA in the long term.