BiQ: Recap for the Week Ending May 2, 2025

Welcome to the BiQ Weekly Recap #15!

I want to welcome the new Biotech iQ members who joined this past week--thank you for joining the BiQ Community. I've been a biotech investor for over two decades, but BiQ is a new service, and I'm humbled and grateful for its warm reception from the biotech community.

If you haven't already done so, I encourage members to join the BiQ Community Chat Server on Discord.

Even if you don't have time to participate regularly, BiQ Chat is still the quickest way to receive updates, trade alerts (Premium only), and answers to questions.

Premium members have access to the Public and Premium channels, while Public members can access the Public channels. Click here for instructions on how to access the BiQ Community Chat Server.

While I publish several articles and updates each week, please remember that Biotech iQ is much more than a newsletter service. BiQ's most valuable tools are found on the Biotech iQ website (www.biotechiq.com). These include:

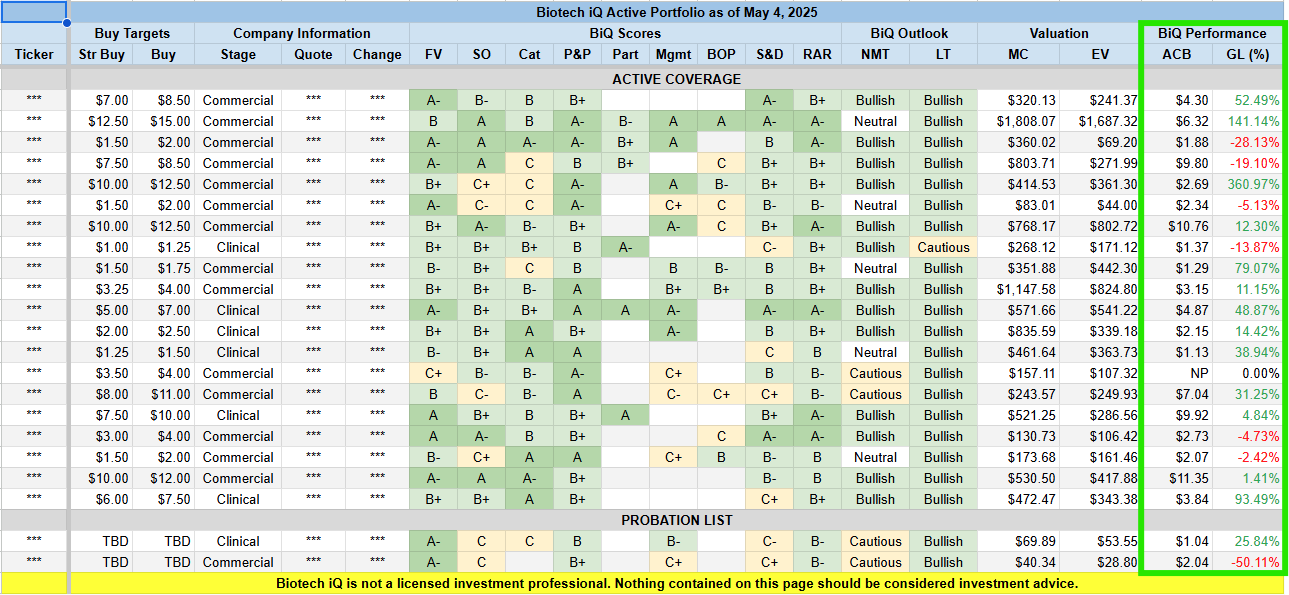

- The Active Portfolio displays a list of all companies currently included in Active Coverage, together with their outlook and ratings.

- The Catalyst Tracker & Events Calendar displays a quarter-by-quarter list of upcoming catalysts and a calendar of forthcoming events.

- The News Feed displays an RSS feed of all press releases from companies covered at Biotech iQ (if the company provides RSS services).

- BiQ Community Chat

Weekly Overview

It was another good week for the XBI. The index closed last Friday at 80.24, opened Monday at 80.72, and closed Friday at 83.47 for a weekly gain of 4.03%. It reached an intra-week high of 84.23 and a low of 80.35 for an intra-week range of 4.83%.

Zooming out to the one-month chart, the index looks constructive as we put the early April volatility further behind us. As a reminder, there were two main drivers of the volatility in April: 1) tariff announcements, and 2) disruptions at the FDA. While I am happy to see the XBI starting to recover, in my opinion, we still have a long way to go before we're clear of these headwinds. Trade negotiations continue to dominate the headlines, and while volatility has subsided, there is still no resolution on tariffs--especially with our most important trading partner, China. As for the FDA, while Dr. Marty Makary gave an interview that seemed intended to soothe biotech investors' nerves, there are still a lot of unknowns. It will take time to work through these uncertainties. I continue to maintain elevated liquidity levels and sell Call options where they make sense.

Zooming out further to the five-year chart, we can see that the index bounced on high volume from the 66-ish level, almost reaching 5-year lows near 64. The RSI has also recovered from heavily oversold conditions and appears to be in a healthy range. From this perspective, I feel cautiously optimistic that the worst damage might be behind us; however, I would prefer to see a few more weeks with high-volume green bars on the chart. As I mentioned above, I plan to remain on defense for now and hold excess liquidity until we see a confirmed uptrend.

During periods of high volatility, it's more important than ever to remember a few fundamental principles:

- The US biotech industry remains as innovative and dynamic as ever, only at much more attractive valuations than we've seen for a while.

- Despite disruptions at the FDA, I believe the agency remains committed to fostering innovation, though there may be some bumps along the way. The US biotech industry remains the envy of the world, and it's in no one's interest to change that.

- Over the long term, companies will continue to trade on fundamentals. Buying quality stocks when they're cheap and selling when they're expensive is still a winning strategy for long-term investors.

That said, proper risk management is critical to long-term success and to avoid the permanent destruction of capital, especially in times of increased market volatility. This means maintaining adequate liquidity reserves to remain rational and focused while others panic.

While I expect volatility may be the new normal for the foreseeable future, I am cautiously optimistic that market conditions will soon begin to stabilize; however, I still plan to maintain a more defensive posture until there are clear signs of a trend reversal.

With regards to trading, I am happy with my current portfolio composition. I continue to sell covered calls where appropriate and have only been adding cautiously to high-conviction names, primarily by using deep OTM puts to take advantage of discounted pricing while maintaining some extra downside protection.

Biotech Industry News & Commentary

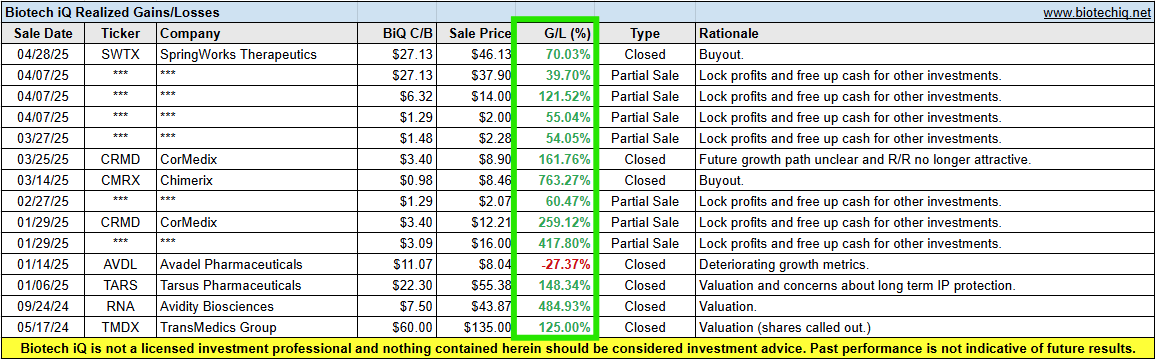

As many investors are aware, Merck KGaA finalized its purchase of SpringWorks Therapeutics (SWTX) for $47/sh early last week. Judging from the posts across Social Media, many investors were very disappointed by the buyout price. For myself, I first entered SWTX at $20/sh and averaged up to around $27/sh over time—never buying shares above what I considered to be a fair and rational valuation. While I admit I would have preferred to see a better buyout price, I also think there are a lot of important lessons to be learned from this recent transaction--and many others like it.

From what I can tell, many biotech investors still seem to be waiting for a return of the "good old days" when marginal companies sold for 3-5x (or more) of their potential peak earnings, and they see the current biotech environment as artificially depressed. However, I'm not sure we'll ever see a return to those kinds of valuations. And in all honesty, I don't think that's necessarily such a bad thing.

First, I do think there are several headwinds facing biotech at the moment. At the risk of stating the obvious, the biggest near-term headwinds are probably uncertainties around tariffs and the global economy, as well as continuity and stability at the FDA. The industry is also grappling with uncertainties around drug pricing. I think these are all valid concerns, and it will take time to work through the issues. However, putting drug pricing and the FDA aside for a moment, tariffs and global economic uncertainties are not specific to biotech, which is why I continue to expect higher-than-average broad market volatility until we have more clarity. I expect tariffs will have a near-term impact, but companies and supply chains will quickly adjust. I don't expect pharma tariffs to be a significant issue for biotech over the long term. As for the global economy and concerns about a possible recession, while this is a legitimate macro concern, biotech is also somewhat insulated since most biotech spending tends to be non-discretionary.

Regarding the disruptions at the FDA, I expect the agency and the industry will work through these issues as well. The US biotech industry remains strategically important for the US, and I firmly believe no one wants to kill this particular goose--whatever the politically motivated narrative of the moment may be. I expect biotech will remain as vital and dynamic as it has always been, and I believe the FDA will find its footing and continue to enable innovation across the industry. If we try to separate the politics from the reality, we may even discover that change could eventually lead to improvement.

Drug pricing is probably a somewhat more complicated issue, and probably the one with the greatest potential long-term impact. However, it's important to remember that the President's recent Executive Order only laid out a series of directives requesting Congress, HHS, and the FDA to explore avenues to potentially bring down drug prices. These are only directives to generate proposals, not actual proposals. Until we know more, it's premature to form any conclusions. I also think that many of the ideas in the EO could be positive for the industry, such as the focus on reducing the clout of PBMs, drug pricing transparency, and improving access to generics and biosimilars. I think it would be very interesting to find out what US drug prices look like if PBM and other middlemen's profits are squeezed out of the system. In fact, we are already seeing many innovative biotech companies start to rebel against the PBM gatekeepers by exploring alternative, DTC strategies. I expect this trend to continue, which could result in potential benefits for drug companies as well as patients.

Change is scary, but that doesn't mean it's bad. There will be some winners and some losers, which makes careful stock-picking and strategic positioning more important than ever. For example, it is my belief that increased patient access to low-cost generics and biosimilars would be healthy for the industry, allowing bio-dollars to be reallocated to more innovative companies with solid data. But I don't think this can happen without taking on the PBMs, since the PBMs are currently the gatekeepers to drug access. Increased access to low-cost generic drugs would run contrary to PBM interests and profit margins. Another loser in such a scenario could be drug manufacturers that rely on marketing expensive, branded versions of generic drugs, which are currently favored by PBMs over low-cost, unbranded generics. On the other hand, companies developing new, innovative drugs could stand to benefit from this shift. The point is, we don't know what will happen or how it will unfold. Rather than reacting with fear, investors should find ways to optimally position themselves to take advantage of the changes as they unfold by remaining calm, logical, and strategic.

Getting back to biotech valuations, I do think some of the previous valuations many biotech investors may be used to are a thing of the past. Not because pharma is less valuable, but because buyers have become more selective. I think valuations going forward will be more rational, and there are many very legitimate reasons for this. Many of the inflated buyouts of the past didn't work out so well for the buyers, and buyers have learned from the experience. There is also a lot more competition than there used to be, not only within the US, but from innovative ex-US companies as well.

So what does this mean for biotech investors? I think it means that the potential for outsized profits is still there, but investors will need to be more rational and discerning. I've been a biotech investor for over two decades, and as I look across the biotech space, I see a lot of attractive companies at very attractive valuations, but I also see a lot of what I consider to be zombie companies that investors continue to chase for the wrong reasons. I think the potential to make outsized returns remains, but careful and rational stock-picking will be increasingly critical.

BiQ In-Progress

I'm adding this new section (though I'm still working on a better title) to the Weekly Recap to give readers a quick preview of what to expect over the next few weeks. Due to a busy travel and work schedule, I haven't been able to write as much as I'd like over the past month and have focused my time on the names in the BiQ Active Portfolio; however, I hope to return to publishing more articles in the weeks ahead. Here are some of the projects I'm currently working on.

- Deep dive analysis of Gossamer Bio (GOSS). I have been working on a comprehensive report on Gossamer Bio and hope to have it published over the next two weeks. Gossamer management has been great about answering my questions; however, I am still awaiting responses from other companies in the space. Once complete, I plan to make the report available to BiQ Premium Members first and release a version for non-Premium subscribers approximately two weeks later.

- I am in the process of evaluating two new names for the BiQAP. Premium subscribers will be notified if and when the new tickers are added.

- In addition to the feature article on GOSS, I am also planning informal BiQ Journal articles for several early-stage names that I find interesting, but which perhaps aren't derisked enough to add to the BiQAP. Some companies I'm considering include LCTX, NMTC, LYEL, and ELDN.

BiQ Service Updates

- The issue with the Events Calendar seems to have (mostly) been fixed. If the calendar spins longer than 15-20 seconds before loading, try advancing to the next month, letting the events load, and then returning to the previous month.

- I am testing a new subscription service to retrieve up-to-date company and market data. The new service offers institutional-level data, hopefully allowing me to update my spreadsheets (which inform the published BiQAP) in real time and perform more in-depth fundamental analysis in less time. I am in the process of integrating my valuation and metrics spreadsheets with the new data feeds.

- I created a new channel for BiQ Premium Chat members to discuss TA & Swing Trading. I know several members have expressed interest in the past, so hopefully this will be a good place to share TA and Swing Trading ideas.

BiQ Performance

Realized Gains/Losses

Current Open Positions

BiQ Premium Membership Discounts

For subscribers interested in an annual Premium membership to Biotech iQ, I am now offering two new promotions:

- 50% Off your First year: https://www.biotechiq.net/50-off-your-first-year

- 20% Off for Life: https://www.biotechiq.net/20-off-for-life

If you're not ready to sign up for an annual membership, a Premium one-month trial membership is also available for $10 using the link below:

- Try 1 Month of BiQ Premium for $10: https://www.biotechiq.net/first-month-for-10

Click here for more information about Biotech iQ, and to see what's included in a Premium membership, or please visit www.biotechiq.net.

Thank you for subscribing to Biotech iQ and reading this Weekly Recap. Premium Members can continue reading below.