BiQ Journal: Highlighting a Few Names from BiQ Chat 04/19/26

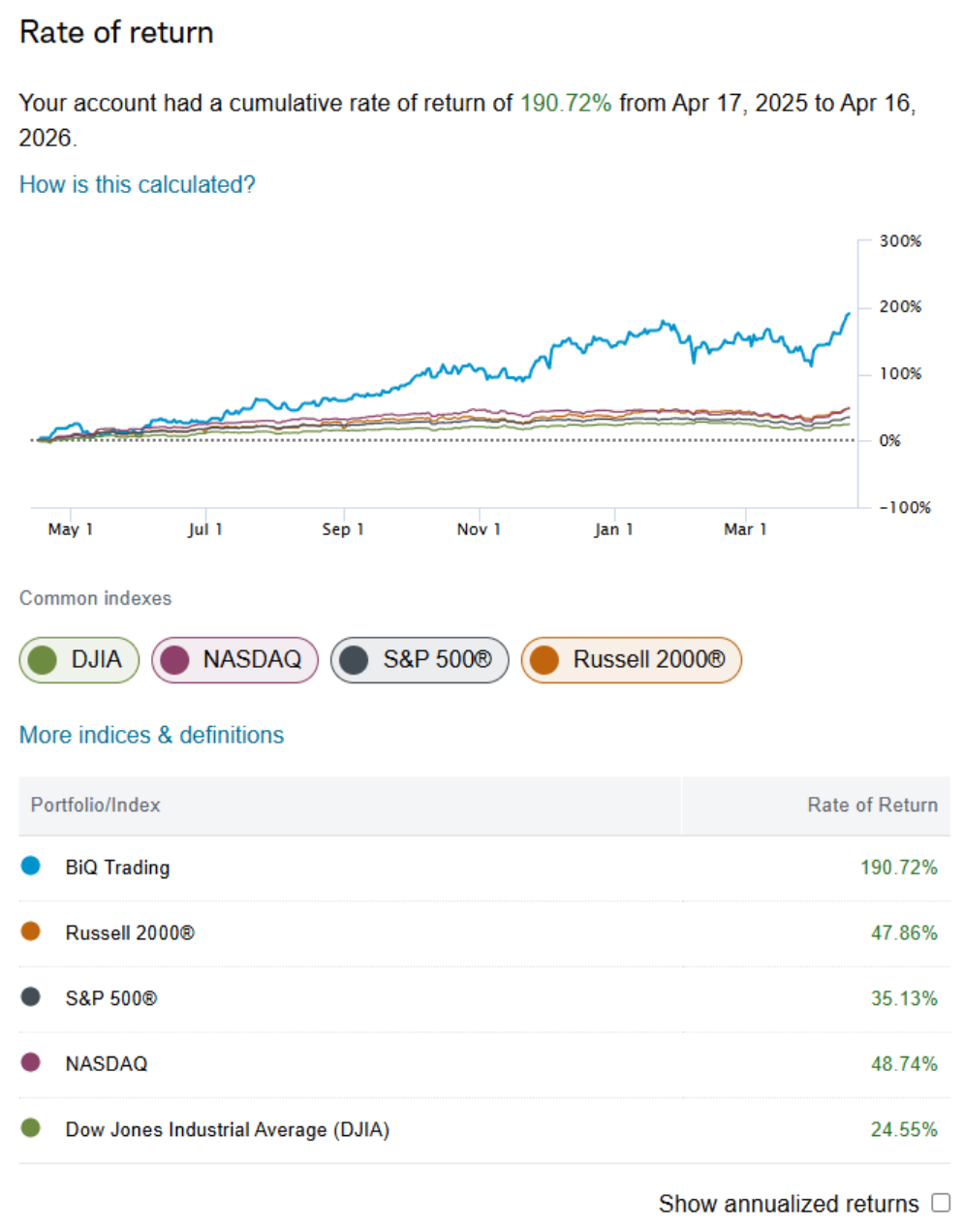

The markets had quite a week, with the major indexes hitting all-time highs on hopes for an Iran peace deal. However, per my article published on April 10th (here), I remain highly skeptical of a peace deal--but I would be happy to be wrong on this one. Either way, this past week was a nice breather. Like the indexes, my personal BiQ portfolio also hit an all-time high, clocking in at a 12-month return of just over 190%. Obviously, the last 5 trading days helped:

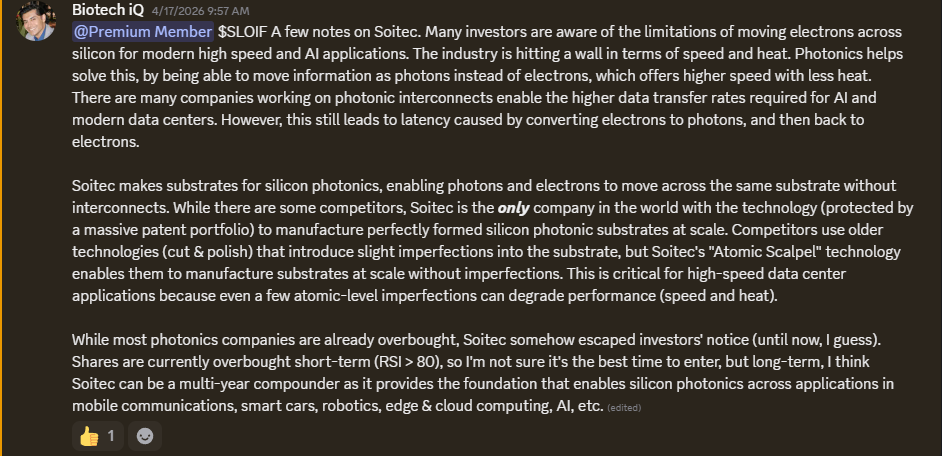

But it wasn't all about war and peace. As one example, I shared a significant new position in Soitec (US ticker SLOIF) with BiQ members via BiQ Chat on April 7th:

To be clear, I am not a market-timer or a momentum trader. At BiQ, I am firmly a long-term value investor; although timing is a consideration, I worry much less about timing than I do about building a solid long-term investing thesis. My investing decisions are driven by careful consideration of valuation, risk, and potential upside, with a sharp focus on attractive companies that may be mispriced and overlooked by the market. Admittedly, however, sometimes I get lucky with timing (and sometimes I don't). Over the intervening 9 trading days, SLOIF ran up by just shy of 100%. Fortunately, I managed to get in just before the market caught on to the story. I also shared further details about the name with BiQ members, and will repost the summary here in case the name is of interest to readers:

Along with SLOIF, I also shared another new position in a very promising European biotech/medtech company that I have been looking into, which rose nearly 20% during the week but pulled back on Friday, closing just shy of 7% above my entry price. I expect both of these to be multi-year compounders, but as always, only time will tell. I have been actively searching for solid ex-US opportunities to improve my global diversification, so I have added these two names to my stable of promising ex-US companies. Hopefully, there will be more to come.

Obviously, past performance is no guarantee of future results (sorry, had to be said!)

Hims & Hers (HIMS) is another position I recently added to. In broad strokes, my thesis is that telehealth will continue to gain momentum over the long term, especially as telehealth companies more broadly leverage AI capabilities. Amazon has moved aggressively into the space with the launch of Amazon Pharmacy, which is definitely a risk factor (as well as a validation of the thesis, to be honest) I will be keeping an eye on. However, even if Amazon becomes, well, the "Amazon" of telehealth, I think there will still be significant space for other players offering a more concierge-level of service. I think HIMS is well-positioned to capitalize on this long-term trend, as well as on the potential recategorization of certain wellness peptides–a new initiative being spearheaded by RFK Jr. I believe HIMS could also be an attractive future partner for other pharma companies seeking to open up DTC distribution channels that bypass PBMs.

One thing that did catch the market's (and my) attention was several insider sales over the past couple of months; however, all were based on 10b5-1s filed in 2025 (ranging from March to November). To provide some context, while it is possible for insiders to rescind a previously filed 10b5-1, it's relatively uncommon due to the heavy regulatory consequences and scrutiny it can trigger--which is the last thing HIMS would want, especially now. I plan to keep an eye on further insider activity, but for now, I am not overly concerned. These 10b5-1s were filed well before HIMS settled its dispute with NVO and entered into a partnership agreement. They also came before the recent interest in deregulating certain wellness peptides, which, if it comes to pass, could be a huge tailwind for HIMS.

My adjusted cost basis, taking into account prior trading profits, is well below $0 at ($26.96). Excluding my trading gains, my actual cost basis on shares is $12.70. Shares have run up by nearly 50% over the past week, so I plan to hold for now; however, I may (or may not) add more exposure on any significant pullbacks, as long as the thesis continues to progress. Any news that jeopardizes the long-term thesis could prompt me to trim or exit my position.

Scynexis (SCYX) also released some interesting news recently. On March 31st, the company issued a press release announcing the acquisition of PXL-770, along with a $40M private placement. To provide a little context, back in 2023, Scynexis entered into a potentially lucrative licensing agreement with GSK for its antifungal agent, BREXAFEMME. Despite my general aversion to antibiotic/antifungal development companies, the deal terms were sufficiently attractive versus the valuation at the time, so I opened a position. Since then, however, unanticipated manufacturing issues allowed GSK to significantly alter the terms of the agreement to Scynexis's disadvantage, causing shares to pull back sharply. I've been holding SCYX at a very slight loss and, before the recent announcement, was planning to unload my position on any signs of strength. However, the acquisition of PXL-770 prompted me to change my game plan; I now plan to hold my position pending further data updates.

In short, PXL-770 is a highly selective, direct AMPK activator for the treatment of Autosomal Dominant Polycystic Kidney Disease (ADPKD). Currently, the only approved therapy for ADPKD is Tolvaptan, a V2 receptor antagonist. Despite carrying a REMS requirement and a black-box warning for hepatotoxicity, Tolvaptan, marketed by Otsuka, generates around $1.5B in annual revenue, primarily from the ADPKD indication. PXL-770 has a safety database comprising data from over 250 patients and shows no signs of ALT/AST elevation, no hypoglycemia risk, no evidence of aquaresis, and only mild GI issues (not uncommon for an oral medication).

The main competitor for PXL-770 is Regulus's RGLS8429 (now part of Novartis), a miR-17 inhibitor delivered via bi-weekly subq injection. Safety data have been encouraging, and importantly, the drug demonstrated a .6% reduction in htTKV (vs +2.5% for placebo) in P1/2 trials.

This sets the bar for PXL-770. If 770 can demonstrate a similar or better reduction in htTKV, I expect the shares to rerate significantly. Scynexis plans to launch a P2 trial in Q4 2026 with top-line data expected in the second half of 2027. While PXL-770 is behind RGLS8429 in development, its oral formulation could be a key marketing advantage for patients who prefer the convenience of a daily oral dose over a bi-weekly subq injection. At a current EV of around $20M and an estimated pro forma FDEV of around $100M, the valuation looks attractive relative to the market opportunity. Downside risk is cushioned by the company's antifungal pipeline and the BREXAFEMME partnership with GSK. My current ACB for SCYX is $1.04.

These have been just a few of the non-BiQAP (BiQ Active Portfolio) names discussed in chat this past couple of weeks. Several other very promising names were also discussed (both bio and non-bio), so please review the BiQ Chat forums for more information on these and other active positions.

Please refer to the BiQAP Live spreadsheet on the Active Portfolio page or the iQCS for additional information.

Please note that the BiQ ACB includes any open options positions, which are accounted for using a "worst case scenario" assumption, plus trading profits (and losses) around my core positions.

Not a BiQ Premium member, or have a friend who may be interested? Try BiQ Premium for $50 per month, or $375 (25% off) for the first year.

Biotech iQ is 100% subscriber supported. If you find this information helpful, please spread the word. You can also follow me on X @ Biotech iQ (_Biotech_iQ).

Biotech iQ is not an investment professional, and nothing on this page or this website should be considered investment advice. Please consult with a licensed investment professional as necessary. Past performance is not indicative of future results.

Member discussion