BiQ Journal: Bepirovirsen Raises the Bar, but the Race Isn't Over.

Phase 3 results for bepirovirsen for the treatment of chronic HBV (cHBV) were recently published in the New England Journal of Medicine (link). Developed by GSK and Ionis, bepirovirsen demonstrated a functional cure rate of 19% when combined with standard background nucleoside/nucleotide analogue (NA) therapy, increasing to 26% for patients with a low baseline viral load (HBsAg <1,000 IU/mL).

This is a meaningful advance over existing NA monotherapies, which typically yield a 2% to 5% functional cure rate over the same period, and over Peg-IFNα, which has a one-year functional cure rate of 3% to 7%. Historically, NA/IFN combinations have demonstrated a ~10% functional cure rate at 48 weeks. Additionally, the NA cessation rate—the ability to safely stop NAs at 48 weeks—was ~24% for bepirovirsen, compared with the 10% to 25% range observed with existing NA/IFN regimens. While this represents a significant leap forward over current options, it still falls short of achieving a long-term functional cure for the majority of cHBV patients. Furthermore, bepirovirsen was associated with notable safety events, including 16% Grade 3+ adverse events and 6% ALT flares.

Arbutus Biopharma, a small-cap biotech, is currently advancing imdusiran as a potential best-in-class competitor. In its Phase 2a IM-PROVE I trial, Cohort 1A (imdusiran for 40 weeks + Peg-IFNα for 24 weeks, n=12) demonstrated a 25% functional cure rate across all patients, and a startling 50% in patients with low baseline viral loads. While this represents a small patient cohort, the signal is nonetheless encouraging. Crucially, there were no treatment-related serious adverse events (SAEs) and no evidence of significant ALT elevation.

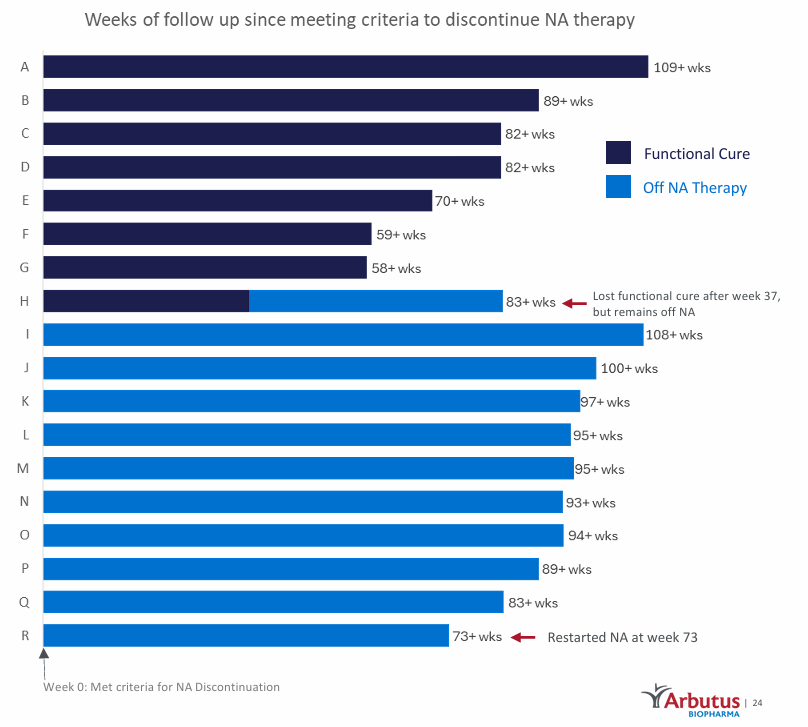

Most promisingly, 100% of the patients who achieved a functional cure maintained undetectable levels of HBsAg at the 24-week follow-up, allowing them to discontinue all NA therapy. Looking at longer-term follow-up data across both the IM-PROVE I and II trials, 94% of patients who stopped NA therapy remained off treatment beyond two years at the most recent data cut-off.

It is worth noting, however, that bepirovirsen’s Phase 3 data reflects its performance as a monotherapy on top of background NA therapy, whereas imdusiran is being evaluated as a combination therapy with Peg-IFNα. GSK explicitly views bepirovirsen as a combination backbone. The company is exploring it sequentially with DAP/TOM (an siRNA licensed from Janssen, originally developed by Arrowhead Pharmaceuticals) and GSK3965193 (a small-molecule antiviral designed to inhibit HBsAg production). While these trials are in earlier stages, safety remains a looming concern. Bepirovirsen demonstrates a clear efficacy step-up, but its associated SAEs and ALT flares raise valid concerns regarding its long-term viability as a combination backbone—especially when compared to imdusiran's clean safety profile.

Arbutus is not standing still, either. Alongside imdusiran, the company is developing AB-101, an oral, liver-targeted PD-L1 inhibitor. The potential advantage of AB-101 over systemic PD-L1 inhibitors is structural: while oncology-focused checkpoint inhibitors exhibit wide systemic availability, AB-101 is designed to concentrate its activity in the liver, mitigating systemic toxicities. If upcoming trials mirror preclinical success, Arbutus likely intends to replace Peg-IFNα with AB-101 to create an entirely oral, safe, and highly effective liver-targeted immune-activating regimen.

Mechanistically, this strategy makes sense. In chronic HBV infection, liver cells secrete a massive, overwhelming volume of Hepatitis B surface antigen. This antigen mass does not just aid viral replication; it acts as an immunosuppressive "smokescreen" that exhausts host T-cells. While an RNAi therapeutic like imdusiran is extremely effective at clearing this HBsAg smokescreen, it lacks the innate architecture to actively rebuild the immune response. To achieve a true functional cure, a therapeutic regimen must clear the viral debris and activate the immune system to take back control. This is why Arbutus pairs imdusiran with Peg-IFNα today, and why it plans to transition to AB-101 in the future.

While the clinical data is ultimately the more important factor to consider, if we look deeper, I think there are also mechanistic reasons why imdusiran is more potent at clearing HBsAg than bepirovirsen. First, imdusiran is an RNAi, whereas bepirovirsen is an ASO: a single-stranded DNA that recruits RNase H to cut a single site on the viral RNA. One ASO degrades one target RNA. Imdusiran is an RNAi, a double-stranded RNA that recruits the RISC complex, which allows a single imdusiran molecule to degrade thousands of target RNA. Second, bepirovirsen targets a single highly conserved binding site. Since HBV mutates rapidly, a specific viral strain with a single-nucleotide mutation could prevent bepirovirsen from binding. However, RNAi therapeutics like imdusiran are inherently more tolerant of small polymorphisms. This is likely why GSK is considering combining bepirovirsen with DAP/TOM: to improve its ability to clear HBsAg.

Imdusiran was recently granted Fast Track Designation (FTD) by the FDA, and Arbutus is actively seeking regulatory alignment on registrational endpoints. If their upcoming, larger Phase 2b placebo-controlled trial maintains the safety and efficacy benchmarks established in IM-PROVE I, the combination of strong data and FTD could provide a viable path toward accelerated approval.

Ultimately, bepirovirsen has proven it can raise the bar for HBV therapeutics, and it stands a strong chance of securing regulatory approval. However, the race for a definitive functional cure is far from over. Imdusiran has produced a compelling clinical signal that positions it well to challenge for best-in-class status. GSK may be in the pole position, but there are many laps left to go.

ABUS share price at time of publication: $4.56

BiQ ACB: $2.75

Please note that the BiQ ACB (adjusted cost basis) includes shares and all open options positions, which are accounted for using a "worst case scenario" assumption, plus realized trading profits (and losses) around my core position.

Not a BiQ Premium member, or have a friend who may be interested? Try BiQ Premium for $50 per month, or $375 (25% off) for the first year.

Biotech iQ is 100% subscriber supported. If you find this information helpful, please spread the word. You can also follow me on X @ Biotech iQ (_Biotech_iQ).

Biotech iQ is not an investment professional, and nothing on this page or this website should be considered investment advice. Please consult with a licensed investment professional as necessary. Past performance is not indicative of future results.

Member discussion